Europe Fixed Wireless Access Market Size and Forecast 2026–2034

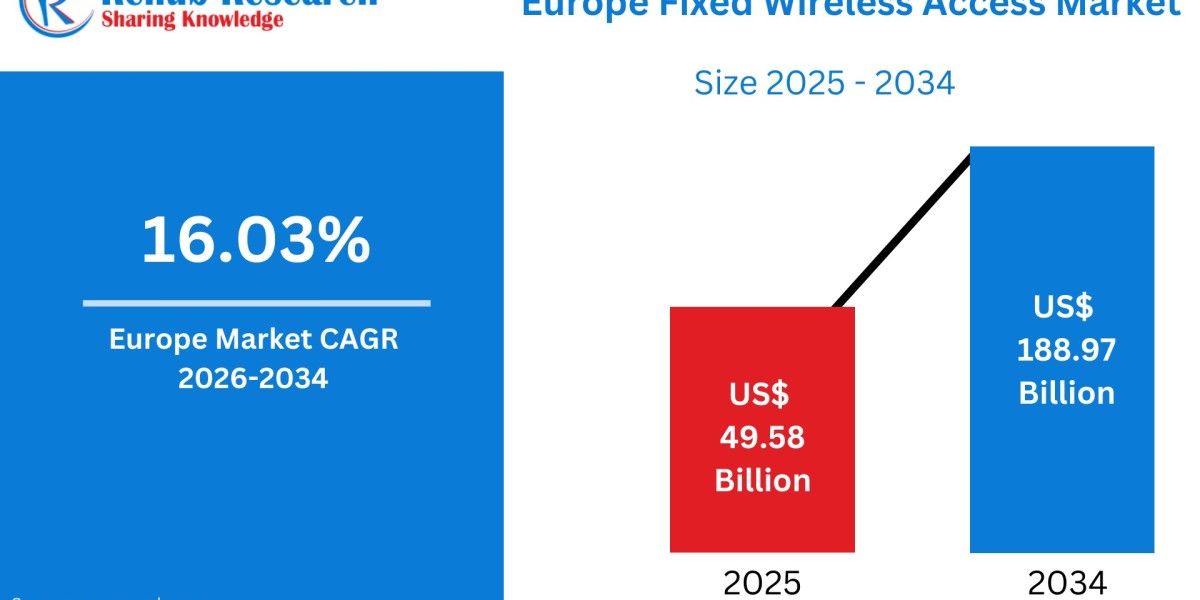

According to Renub Research Europe Fixed Wireless Access (FWA) market is entering a phase of accelerated expansion, driven by the region’s intensifying need for high-speed, affordable, and scalable broadband connectivity. The market is projected to grow from US$ 49.58 billion in 2025 to approximately US$ 188.97 billion by 2034, registering a strong compound annual growth rate (CAGR) of 16.03% during the 2026–2034 period. This rapid growth reflects structural changes in how broadband is deployed across Europe, particularly as governments, telecom operators, and enterprises seek alternatives to fiber that can be rolled out faster and at lower cost. With increasing digitalization, remote work adoption, cloud usage, and smart infrastructure initiatives, FWA is becoming a core pillar of Europe’s broadband strategy.

Download Free Sample Report:https://www.renub.com/request-sample-page.php?gturl=europe-fixed-wireless-access-market-p.php

Europe Fixed Wireless Access Market Overview

Fixed Wireless Access refers to the delivery of broadband internet to homes and businesses using wireless radio links instead of traditional wired infrastructure such as fiber-optic or copper cables. In an FWA deployment, data is transmitted from a nearby base station to a customer’s premises through 4G, 5G, or millimeter-wave (mmWave) technology, using indoor or outdoor customer premises equipment (CPE). Compared with wired broadband, FWA offers significantly faster deployment timelines, lower civil-works costs, and higher scalability, making it especially attractive in areas where fiber installation is slow, expensive, or logistically complex.

Across Europe, FWA adoption is increasing as operators respond to persistent connectivity gaps in rural, semi-urban, and suburban regions. While major cities often benefit from extensive fiber networks, many communities still rely on legacy DSL or cable infrastructure with limited speeds. FWA provides an efficient solution to bridge this digital divide while aligning with national and European Union–level broadband objectives. The rising demand for cloud services, video streaming, e-learning, telemedicine, and remote working further amplifies the need for reliable, high-capacity internet access, reinforcing FWA’s relevance across the continent.

Increasing Demand for Broadband in Underserved and Suburban Areas

One of the most powerful growth drivers of the Europe FWA market is the rising demand for broadband in underserved, suburban, and rural areas. Europe’s demographic landscape combines dense metropolitan centers with wide-ranging rural and semi-rural regions, many of which lack comprehensive fiber coverage. Extending fiber to these areas often involves high trenching costs, lengthy permitting processes, and long deployment cycles. FWA enables operators to bypass these constraints by leveraging licensed and unlicensed spectrum to deliver broadband quickly and economically.

For households and small businesses in outer suburbs and semi-rural communities, FWA frequently serves as a practical upgrade from slow DSL or aging cable connections. The simplified installation process, which avoids in-home excavation and minimizes public right-of-way negotiations, accelerates subscriber acquisition and reduces churn. This demand-driven dynamic makes FWA particularly attractive for regional internet service providers and mobile network operators seeking to monetize existing radio access assets while meeting national broadband targets and consumer expectations for near-symmetric speeds in markets where full fiber penetration remains incomplete.

5G NR and Mid/High-Band Spectrum Enabling Multi-Gbps FWA

The commercialization of 5G New Radio (NR) technology has fundamentally strengthened the value proposition of FWA across Europe. The availability of mid-band spectrum, particularly around 3.5 GHz, along with higher-frequency mmWave bands, enables significantly higher throughput, lower latency, and greater network capacity. These advancements allow operators to offer fixed broadband services that increasingly rival fiber in terms of speed and quality of service.

Technologies such as Massive MIMO, beamforming, and carrier aggregation enhance spectral efficiency and extend coverage for fixed premises. In dense urban corridors, mmWave deployments enable multi-gigabit speeds, while mid-band frequencies provide a balance between coverage and capacity for suburban environments. The use of 5G architecture also supports service-level guarantees and network slicing, enabling operators to segment traffic for enterprise customers and deliver differentiated quality of service. As 5G coverage continues to expand across Europe, its impact on FWA adoption is expected to intensify.

Cost Economics and Speed-to-Revenue for Operators

The favorable cost economics of FWA are a critical driver of market growth. Compared with full fiber rollouts, FWA requires substantially lower upfront capital expenditure due to minimal civil works, simpler CPE installations, and the ability to reuse existing mobile network infrastructure. Operators can enter new markets with limited investment, test demand, and scale capacity incrementally as adoption grows.

Operational efficiencies further strengthen the business case. Remote provisioning, over-the-air software updates, and standardized CPE designs reduce installation and maintenance costs. These advantages are particularly compelling for smaller operators and mobile virtual network operators seeking to differentiate through competitive pricing or bundled services. In regions where public subsidies or rural broadband grants are available, FWA projects can rapidly absorb funding and demonstrate measurable connectivity improvements, accelerating returns on investment.

Spectrum Fragmentation and Regulatory Variability

Despite strong growth prospects, the Europe FWA market faces notable regulatory challenges. Spectrum allocation, licensing frameworks, and channelization policies vary significantly across European countries, complicating cross-border deployments. Operators must navigate a patchwork of licensed, lightly licensed, and unlicensed bands, each with different power limits and coexistence requirements.

This fragmentation increases equipment complexity, as base stations and CPE must support multiple band plans and comply with region-specific certifications. Variability in spectrum auction timelines and licensing conditions can delay network rollouts or force operators into suboptimal frequency bands for fixed coverage. For smaller ISPs and new entrants, regulatory uncertainty raises commercial risk, while larger multi-country operators face constrained economies of scale in procurement and network planning.

Line-of-Sight Constraints and Urban Interference Challenges

Technical limitations related to high-frequency spectrum present another challenge for FWA deployment. While mmWave and higher bands enable very high data rates, they are highly sensitive to propagation conditions. Limited range, susceptibility to foliage, building materials, and weather effects such as rain fade can impact link reliability.

In dense urban environments, reflections, clutter, and co-channel interference require careful radio planning and network densification, which increases deployment costs. Rural deployments face different constraints, including longer distances and physical obstacles that may necessitate higher-gain antennas or relay sites. Indoor signal penetration at higher frequencies is also weaker, often requiring outdoor CPE installations that some consumers may resist for aesthetic reasons. These trade-offs mean that FWA must be strategically deployed rather than treated as a universal substitute for fiber.

Europe Fixed Wireless Access Hardware Market

The hardware segment is a foundational component of the European FWA ecosystem. Key equipment categories include macro and small-cell base stations, indoor and outdoor CPE, antennas, and backhaul solutions. Demand increasingly favors multiband and multimode devices that support both 4G and 5G, along with carrier aggregation and software upgradeability to accommodate regulatory diversity across countries.

Vendors focus on compact, weather-resistant outdoor CPE with integrated high-gain antennas to improve non-line-of-sight performance, as well as simplified self-installation options for consumers. On the network side, virtualization and open RAN–compatible hardware reduce vendor lock-in and support more flexible, disaggregated deployment models. Edge computing capabilities embedded in gateways and CPE further enhance performance for latency-sensitive applications, reinforcing the role of advanced hardware in driving market adoption.

Europe 24–39 GHz Fixed Wireless Access Market

The 24–39 GHz frequency band occupies a strategic middle ground between sub-6 GHz and extreme mmWave spectrum. It offers wide channel bandwidths that support high throughput while maintaining more manageable propagation characteristics than higher frequencies. These bands are particularly suited for suburban deployments and targeted urban use cases where demand density justifies selective densification.

However, deployments in this range still require careful planning due to limited cell radius and reduced indoor penetration. National certification requirements and power limits vary, adding complexity. Typical applications include business parks, new housing developments, and city outskirts where fiber availability is limited. Scalability in this segment depends heavily on spectrum harmonization and vendor support for flexible, multi-band radio platforms.

Europe Urban Fixed Wireless Access Market

Urban FWA deployments focus on dense residential clusters and enterprise zones where high demand supports the cost of network densification. Operators deploy small cells on rooftops, street furniture, and building facades to deliver competitive speeds and low latency. Urban FWA enables premium residential services, smart building connectivity, and enterprise-grade broadband alternatives.

Municipal infrastructure such as smart lighting and public assets helps reduce site acquisition challenges, while advanced interference management and dynamic spectrum sharing are essential in congested radio environments. Urban FWA also enables specialized use cases, including temporary connectivity for events and wireless backup links for critical sites. Operators must balance capital investment with high average revenue per user potential in these markets.

Europe Fixed 5G Wireless Access Market

Fixed 5G Wireless Access combines the capabilities of 5G NR with fixed broadband service models, positioning it as a strategic growth lever for European operators. Bundled offerings that include home broadband, IPTV, and enterprise services are becoming increasingly common, supported by SIM-based provisioning and network slicing for differentiated quality of service.

The 5G architecture enables enterprise applications such as remote offices, retail connectivity, and IoT aggregation, while allowing operators to reuse existing spectrum and infrastructure. Challenges remain in ensuring consistent indoor coverage and integrating fixed services into billing and operational systems. Nevertheless, fixed 5G remains a critical tool for competing with fiber and cable providers at lower incremental cost.

Europe Commercial Fixed Wireless Access Market

Commercial FWA targets business customers ranging from small enterprises to large campuses. Enterprises value FWA for rapid provisioning, predictable latency, and flexibility, using it as a primary connection, backup link, or hybrid solution alongside fiber. Providers differentiate through service-level agreements, managed networking equipment, static IP addresses, and integrated security services.

Verticals such as hospitality, logistics, and temporary retail benefit particularly from FWA’s ability to deliver high-capacity connectivity without long installation lead times. Commercial pricing models typically deliver higher margins due to value-added services and customization.

Germany Fixed Wireless Access Market

Germany represents one of the most significant FWA markets in Europe due to its large population and ambitious broadband targets. While urban cores are well served by fiber and cable, FWA plays a critical role in suburbs, multi-dwelling units, and rural areas where trenching costs are high. Hybrid strategies that combine fiber backbones with wireless last-mile access are common, supported by regulatory emphasis on universal broadband coverage.

United Kingdom Fixed Wireless Access Market

The United Kingdom’s FWA market is driven by rural connectivity goals and competitive pressure in urban areas. Fixed wireless complements fiber rollouts in remote regions and islands, while urban deployments focus on business continuity and high-capacity services. Government voucher schemes and regulatory support continue to stimulate adoption.

Netherlands Fixed Wireless Access Market

In the Netherlands, strong fiber penetration shapes a niche FWA market focused on suburbs, temporary demand, and enterprise connectivity where fiber is constrained. Progressive municipal policies and smart-city infrastructure facilitate small-cell deployments, making the country a testing ground for innovative FWA service models.

Europe Fixed Wireless Access Market Segmentation

The Europe FWA market is segmented by type into hardware and services. By operating frequency, it includes sub-6 GHz, 24–39 GHz, and above 39 GHz bands. Demographic segmentation covers urban, semi-urban, and rural areas, while technology segmentation distinguishes between 4G and 5G. Applications include residential, commercial, industrial, and government use cases across major European countries.

Competitive Landscape of the Europe Fixed Wireless Access Market

The competitive landscape of the Europe Fixed Wireless Access market features a mix of global telecom equipment vendors, mobile network operators, and specialized wireless solution providers. Key companies active in the market include Nokia Corporation, AT&T Inc., T Mobile USA, Inc., CommScope Inc., Verizon Communications Inc., Vodafone Group Plc., Huawei Technologies Co., Ltd., Inseego Corp., Telstra, and FS.com. These players compete through network innovation, hardware advancements, partnerships, and strategic investments, shaping the future of FWA deployment across Europe through 2034.