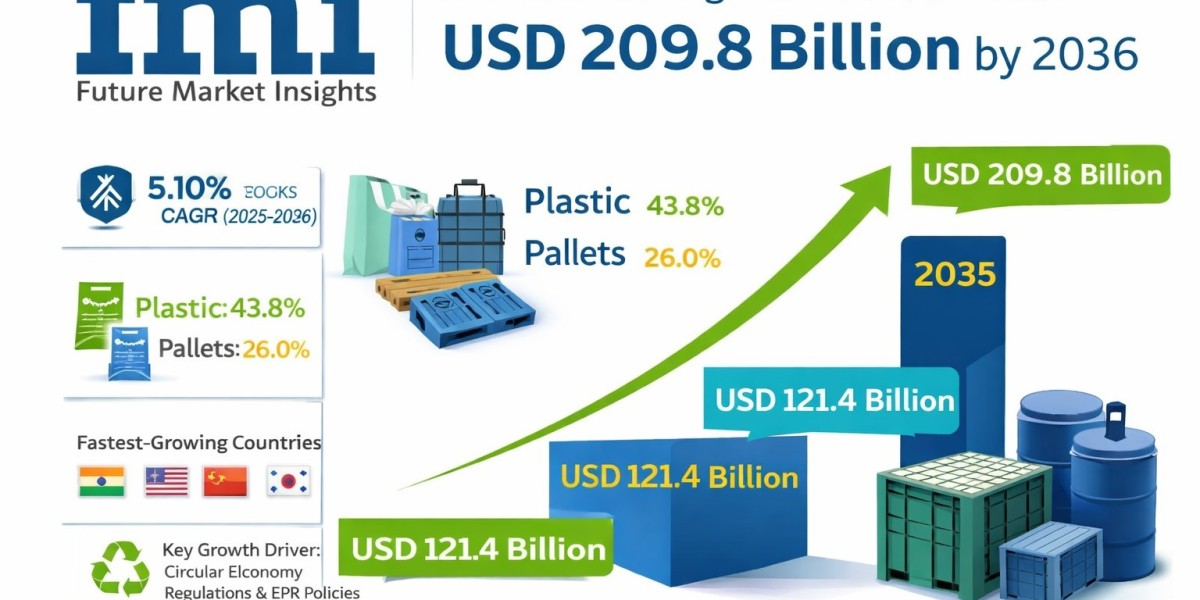

The global reusable packing market is witnessing steady structural growth as industries transition away from single-use transit packaging toward durable and trackable supply chain assets. The market was valued at USD 121.4 billion in 2025 and is projected to reach USD 127.6 billion in 2026, ultimately expanding to USD 209.8 billion by 2036, reflecting a 5.10% CAGR during the forecast period.

Quick Stats: Reusable Packing Market (2025–2036)

• Market Value (2025): USD 121.4 Billion

• Forecast Value (2036): USD 209.8 Billion

• CAGR: 5.10%

• Leading Segment: Plastic Material (43.8% Share)

• Key Product Segment: Pallets (26.0% Share)

• Fastest-Growing Countries: India, United States, China, South Korea, Japan

• Key Growth Driver: Regulatory mandates promoting reusable packaging systems and reverse-logistics networks

Structural Growth Driver: Circular Economy Regulations and Extended Producer Responsibility

Governments worldwide are introducing stringent environmental regulations targeting single-use plastics and packaging waste. Regulatory frameworks such as extended producer responsibility (EPR) policies shift the responsibility of waste management from municipalities to manufacturers, encouraging companies to adopt reusable packaging systems. These policies significantly influence procurement decisions across logistics, retail, and manufacturing sectors.

Key regulatory and industry frameworks include:

• Recycling and circular economy regulations

• Extended Producer Responsibility (EPR) mandates

• Packaging reuse targets and compliance frameworks

• Sustainable material certification requirements

• Supply chain traceability standards

From Compliance to Industry Transformation

The reusable packing industry is evolving from regulatory compliance toward a broader operational transformation across global supply chains. Businesses are adopting closed-loop logistics networks where containers, pallets, and crates circulate repeatedly within distribution systems rather than being discarded after a single trip.

Companies are prioritizing:

• Sustainability performance and waste reduction

• Cost efficiency through shared asset pooling

• Recyclability and material lifecycle management

• Operational compatibility with automated logistics systems

• Traceability and regulatory compliance

Technology Transformation: Smart Logistics and Trackable Packaging Systems

Technological innovation is playing a critical role in advancing reusable packing systems. Modern packaging fleets increasingly integrate RFID tags, IoT sensors, and digital asset tracking software, allowing operators to monitor packaging location and condition throughout the supply chain.

Key innovation areas include:

• Advanced material development for long-life transit containers

• Automation integration with warehouse logistics systems

• Lightweight packaging design for transportation efficiency

• Sustainable material engineering using recycled polymers

• Manufacturing efficiency improvements through injection-molding technologies

Segment Highlights

By Material Type

• Plastic (43.8% Share): Lightweight, durable polymers dominate reusable transport packaging due to their sanitation resistance and long operational lifespan.

• Metal: Preferred for heavy-duty industrial applications where extreme durability is required.

• Wood: Traditionally used for pallets but gradually declining due to regulatory and sustainability pressures.

• Glass: Utilized in specialized applications requiring chemical resistance and product protection.

• Others: Composite materials and hybrid formats used in niche logistics environments.

By Product Type

• Pallets (26.0% Share): Core structural units for warehouse automation and transport logistics.

• Crates: Widely deployed in food distribution and retail supply chains.

• Intermediate Bulk Containers (IBCs): Used for transporting liquids and industrial materials.

• Drums & Barrels: Essential for chemicals, lubricants, and hazardous material transportation.

• Others: Specialty reusable containers designed for specific supply chain applications.

Regional Outlook: Emerging Economies Drive Adoption

Global demand for reusable packing solutions is increasing as regulatory frameworks and supply chain modernization accelerate. Developed markets are implementing strict sustainability mandates, while emerging economies are adopting reusable logistics systems to reduce material waste and improve transportation efficiency.

Country-level growth projections include:

• India (5.6% CAGR): Expansion driven by waste conversion programs and modernization of agricultural supply chains.

• China (5.3% CAGR): Export-driven manufacturing requires durable and trackable logistics packaging.

• United States (5.4% CAGR): Federal sustainability initiatives and reverse-logistics infrastructure support adoption.

• South Korea (5.2% CAGR): High-tech manufacturing industries require contamination-controlled reusable containers.

• Germany (4.6% CAGR): Strong circular economy regulations accelerate reusable packaging deployment.

Risk Landscape: Market Constraints and Challenges

Despite strong growth prospects, the reusable packing market faces operational and financial challenges associated with reverse logistics infrastructure and asset management complexity. Smaller companies often struggle to manage return logistics and asset tracking systems required for reusable packaging networks.

Key market challenges include:

• Raw material price volatility

• Supply chain disruptions affecting return logistics

• Infrastructure gaps in reverse-logistics networks

• Regulatory complexity across regions

• High manufacturing and tracking technology costs

Competitive Landscape: Key Market Players

The reusable packing industry is moderately consolidated, with leading companies focusing on asset pooling networks, logistics software integration, and sustainable material innovation. Market participants are expanding geographic coverage and investing in digital asset management platforms to strengthen their competitive positions.

Top key companies include:

• Brambles (CHEP)

• Tosca Ltd.

• Nefab Group

• Schoeller Allibert

• Schütz GmbH & Co. KGaA

Other notable companies include Myers Industries, Menasha Corporation, Re-Zip, Horen Group, and Egee Pallet.

Outlook: Future of the Reusable Packing Market

The future of the reusable packing market will be shaped by regulatory enforcement, supply chain digitalization, and circular economy initiatives. As industries transition toward sustainable logistics models, reusable packaging solutions will become central to global distribution systems.

Key growth drivers expected to shape the market include:

• Technology advancement in smart packaging tracking

• Sustainability initiatives and circular economy policies

• Manufacturing expansion of reusable packaging fleets

• Supply chain innovation and logistics digitization

For an in-depth analysis of evolving industry trends and to access the complete strategic outlook for the market through 2036, visit the official report page at: https://www.futuremarketinsights.com/reports/reusable-packing-market