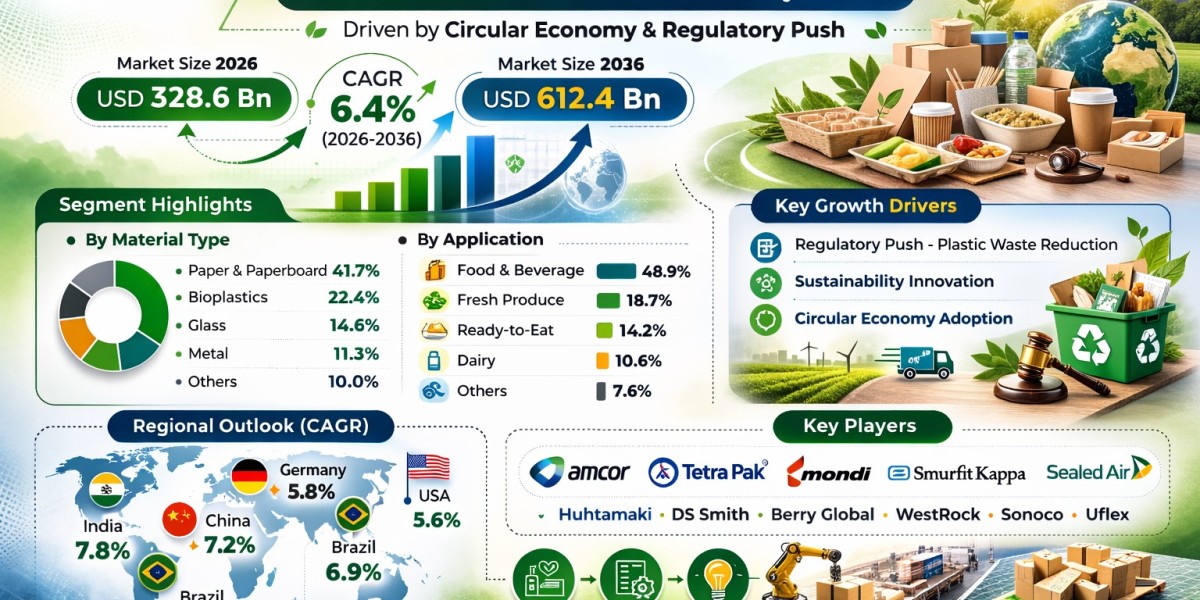

The global sustainable food packaging market is witnessing robust expansion as industries increasingly transition toward eco-friendly and recyclable packaging solutions. The market is estimated to reach a value of USD 328.6 billion in 2026 and is projected to grow to approximately USD 612.4 billion by 2036, registering a CAGR of 6.4% during the forecast period. This growth trajectory is driven by rising environmental concerns, evolving consumer preferences, and stringent regulatory mandates targeting plastic waste reduction.

Quick Stats: Sustainable Food Packaging Market (2026–2036)

• Market Value (2026): USD 328.6 Billion

• Forecast Value (2036): USD 612.4 Billion

• CAGR: 6.4%

• Leading Segment: Paper & Paperboard Packaging – 41.7% share

• Key Product Segment: Flexible Packaging – 36.5% share

• Fastest-Growing Countries: India, China, Brazil, Germany, United States

• Key Growth Driver: Regulatory push for reduction of single-use plastics

Structural Growth Driver: Regulatory Push for Sustainable Packaging

The primary growth driver for the sustainable food packaging market is the increasing implementation of environmental regulations aimed at reducing plastic waste. Governments across regions are enforcing bans on single-use plastics and introducing extended producer responsibility (EPR) frameworks, pushing manufacturers toward sustainable alternatives. These regulations are reshaping material selection, packaging design, and supply chain operations.

Key regulatory and industry standards include:

• Recycling regulations and waste management mandates

• Compostability and biodegradability certifications

• Material sustainability and lifecycle assessment guidelines

• Food safety and packaging compliance standards

From Compliance to Industry Transformation

The sustainable packaging shift is no longer limited to compliance; it is evolving into a core industry transformation. Companies are redesigning packaging formats to reduce material usage, improve recyclability, and optimize logistics efficiency. This shift is fostering innovation across the value chain, from raw material sourcing to end-of-life disposal.

Key industry priorities include:

• Sustainability performance optimization

• Cost-efficient material usage

• Enhanced recyclability and reuse potential

• Compatibility with existing production systems

Technology Transformation: Advanced Sustainable Material Innovation

Technological advancements are playing a crucial role in shaping the future of sustainable food packaging. Innovations in material science are enabling the development of high-performance biodegradable and bio-based materials that offer durability and barrier properties comparable to traditional plastics.

Automation and smart manufacturing processes are improving production efficiency while reducing waste generation. Additionally, advancements in lightweight packaging design are minimizing resource consumption and transportation costs.

Key innovation areas include:

• Advanced bio-based material development

• Automation integration in packaging production

• Lightweight and minimalistic packaging design

• Sustainable material engineering

• Manufacturing efficiency improvements

Segment Highlights

By Material Type

• Paper & Paperboard (41.7% share): Widely adopted due to recyclability and cost-effectiveness

• Bioplastics (22.4% share): Growing demand for compostable alternatives

• Glass (14.6% share): Preferred for premium and reusable packaging

• Metal (11.3% share): High durability and recyclability

• Others (10.0% share): Includes hybrid and innovative materials

By Application

• Food & Beverage Packaging (48.9% share): Dominates due to high consumption volume

• Fresh Produce Packaging (18.7% share): Focus on extending shelf life sustainably

• Ready-to-Eat Meals (14.2% share): Rising convenience food demand

• Dairy Packaging (10.6% share): Emphasis on hygiene and preservation

• Others (7.6% share): Includes niche and specialty applications

Regional Outlook: Emerging Economies Drive Adoption

Global demand for sustainable food packaging is expanding across both developed and emerging economies, with Asia-Pacific and Latin America leading growth due to increasing urbanization and regulatory adoption. Developed markets continue to focus on innovation and circular economy integration.

• India (7.8% CAGR): Strong policy push and rising eco-conscious consumers

• China (7.2% CAGR): Large-scale manufacturing and regulatory enforcement

• Brazil (6.9% CAGR): Growing food export sector driving demand

• Germany (5.8% CAGR): Advanced recycling infrastructure and sustainability focus

• United States (5.6% CAGR): Corporate sustainability initiatives accelerating adoption

Risk Landscape: Market Constraints and Challenges

Despite strong growth potential, the market faces several structural and operational challenges that may impact scalability and profitability.

• Raw material price volatility

• Supply chain disruptions

• Limited recycling infrastructure in emerging regions

• Regulatory complexity across global markets

• High manufacturing and transition costs

Competitive Landscape: Key Market Players

The sustainable food packaging market is highly competitive, with companies focusing on innovation, partnerships, and capacity expansion to strengthen their market position. Strategic investments in R&D and sustainable material development are key differentiators among leading players.

Top 5 key companies:

• Amcor Plc

• Tetra Pak International S.A.

• Mondi Group

• Smurfit Kappa Group

• Sealed Air Corporation

Other notable companies include Huhtamaki Oyj, DS Smith Plc, Berry Global Inc., WestRock Company, Sonoco Products Company, and Uflex Ltd.

Outlook: Future of the Sustainable Food Packaging Market

The future of the sustainable food packaging market is expected to be defined by continuous innovation, regulatory alignment, and circular economy integration. Companies that successfully balance sustainability with cost efficiency and performance will gain a competitive advantage.

Key future growth drivers include:

• Technology advancement in eco-materials

• Expansion of sustainability initiatives

• Manufacturing capacity expansion

• Supply chain innovation and optimization

For an in-depth analysis of evolving industry trends and to access the complete strategic outlook for the market through 2036, visit the official report page at: https://www.futuremarketinsights.com/reports/smart-tag-packaging-market-share-analysis