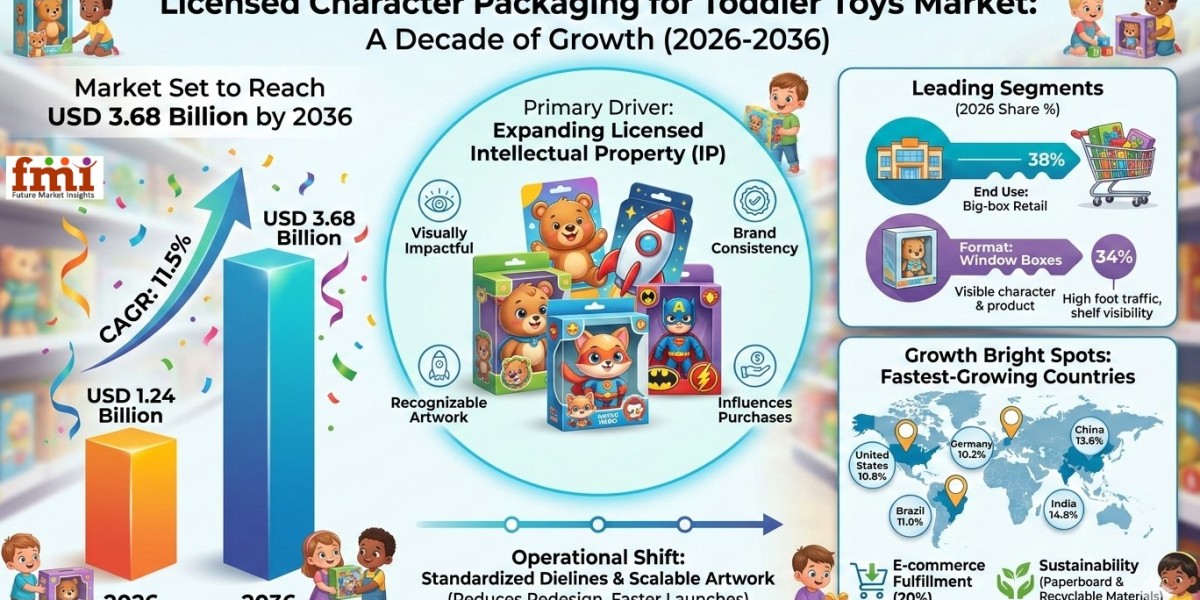

The global Licensed Character Packaging for Toddler Toys Market is estimated to reach USD 1.24 billion in 2026 and is projected to grow significantly to USD 3.68 billion by 2036, expanding at a CAGR of 11.5% during the forecast period. Market expansion is primarily driven by the rising monetization of licensed intellectual property (IP) across toddler toy portfolios, where packaging serves not only as a protective format but also as a key merchandising interface that influences consumer purchasing decisions in retail environments.

Industry transformation is increasingly tied to the operational role of packaging within licensed toy programs. Packaging architectures are shifting toward standardized dielines and scalable artwork systems that enable licensors and brands to deploy character portfolios across multiple SKUs, retailers, and geographic markets without repeated redesign cycles. As licensed character programs refresh frequently, packaging suppliers capable of delivering consistent print fidelity, structural stability, and regulatory-compliant labeling systems are becoming strategically valuable across global toy supply chains.

Quick Stats: Licensed Character Packaging for Toddler Toys Market (2026–2036)

• Market Value (2026): USD 1.24 Billion

• Forecast Value (2036): USD 3.68 Billion

• CAGR: 11.5%

• Leading Segment: Big-box Retail End Use (38% Share)

• Key Product Segment: Window Boxes (34% Share)

• Fastest-Growing Countries: India, China, Brazil, United States, Germany

• Key Growth Driver: Expansion of licensed IP-driven toy portfolios and packaging-based retail merchandising

Structural Growth Driver: Expansion of Licensed Intellectual Property in Toddler Toy Categories

The primary structural driver shaping the licensed character packaging market is the increasing commercial value of licensed entertainment characters within toddler toy portfolios. Character-driven products rely heavily on packaging as a visual merchandising tool, where recognizable artwork, color accuracy, and brand consistency directly influence shelf visibility and consumer engagement. As licensors continue to expand character franchises across global markets, packaging demand increases in parallel with SKU expansion.

Regulatory oversight is also reinforcing disciplined packaging execution for products targeted at young children. Compliance requirements related to labeling, safety warnings, and age grading require packaging systems capable of delivering consistent communication across multiple retail channels. In regions such as North America and Europe, stricter toy safety standards and warning communication requirements are increasing the value of standardized packaging platforms that reduce execution errors and maintain regulatory compliance.

Growing complexity in retail distribution further strengthens demand for scalable packaging architectures that maintain consistency across physical stores and e-commerce fulfillment environments.

Key regulatory and industry frameworks include:

• Toy safety labeling regulations

• Choking hazard and small-parts warning requirements

• Product traceability and documentation standards

• Material safety and sustainability compliance guidelines

• Packaging performance standards for children’s products

From Compliance to Industry Transformation

Licensed character packaging is transitioning from a simple protective function to a strategic component of retail conversion and brand governance. Packaging now serves as a critical interface where licensors enforce brand guidelines, ensure artwork consistency, and maintain compliance across global retail programs.

Manufacturers and packaging suppliers are increasingly adopting standardized packaging platforms that allow character programs to scale efficiently. By using repeatable dielines and modular artwork zones, companies can rapidly refresh character portfolios while maintaining structural consistency across product lines. This approach reduces redesign cycles and accelerates product launches across different markets and retailers.

Industry priorities are increasingly centered on operational performance and brand integrity.

Companies are focusing on:

• Sustainability performance

• Cost efficiency in high-volume production

• Recyclable and paperboard-based packaging solutions

• Operational compatibility with mass retail distribution

• Omnichannel-ready packaging durability

Technology Transformation: High-Fidelity Print and Structural Packaging Engineering

Technological advancement in printing and packaging conversion is playing a major role in enabling licensed packaging programs to scale efficiently. Character artwork requires high color fidelity, precise graphic reproduction, and durable surface finishing to maintain brand integrity through handling, transportation, and retail display.

Modern packaging manufacturing technologies are enabling higher levels of print accuracy and structural reliability across large production runs. Automation in die-cutting, digital color management systems, and advanced coatings are improving packaging consistency while reducing defects and production variability.

Key innovation areas include:

• Advanced material development for high-print-quality substrates

• Automation integration in carton converting processes

• Lightweight structural packaging design

• Sustainable material engineering

• Manufacturing efficiency improvements

Segment Highlights

By End Use

• Big-box Retail (38% share): Dominates due to high product throughput and strong shelf-visibility requirements that favor visually impactful licensed packaging.

• Specialty Toy Stores (22% share): Emphasize premium presentation and brand storytelling through packaging design.

• E-commerce Fulfillment (20% share): Growth driven by demand for durable packaging capable of protecting both product and printed artwork during shipping.

• Convenience Retail Channels (12% share): Require compact packaging formats that maintain brand visibility in limited display spaces.

• Gift Retail Channels (8% share): Packaging plays a strong role in impulse purchase behavior and gifting appeal.

By Packaging Format

• Window Boxes (34% share): Combine character artwork with direct product visibility, enhancing consumer trust and purchase conversion.

• Folding Cartons (28% share): Provide cost-effective and scalable packaging solutions for mass retail programs.

• Blister Packaging (18% share): Common for smaller toy items requiring strong product protection.

• Clamshell Packaging (12% share): Offers enhanced durability and tamper resistance.

• Hybrid Paperboard Packs (8% share): Emerging formats combining visual appeal with structural protection.

Regional Outlook: Emerging Economies Drive Adoption

Global growth is increasingly distributed across both mature and emerging toy markets. While North America retains the largest share due to strong licensed-IP penetration and large-scale retail distribution networks, emerging economies are experiencing rapid growth as organized retail expands and licensed character adoption increases among younger consumers.

Country-level CAGR projections include:

• India (14.8% CAGR): Fastest growth driven by expanding organized retail and rising licensed character penetration.

• China (13.6% CAGR): Growth supported by large-scale toy manufacturing and rapid character program refresh cycles.

• Brazil (11.0% CAGR): Increasing adoption of licensed toys across mainstream retail channels.

• Germany (10.2% CAGR): Strong compliance-driven packaging governance under evolving EU toy safety standards.

• United States (10.8% CAGR): Large retail networks and strong licensing culture sustain market expansion.

Risk Landscape: Market Constraints and Challenges

Despite strong growth prospects, the market faces operational and regulatory challenges linked to licensing governance, supply chain complexity, and production standardization requirements.

Key risks include:

• Raw material price volatility

• Supply chain disruptions affecting paperboard supply

• Infrastructure gaps in emerging markets

• Regulatory complexity in children’s product labeling

• High manufacturing costs for high-fidelity licensed packaging

Competitive Landscape: Key Market Players

Competition in the licensed character packaging sector is primarily driven by packaging execution capability, print accuracy, and standardized packaging platform development. Suppliers that can deliver licensing-grade print fidelity, consistent structural performance, and omnichannel-ready packaging solutions are gaining competitive advantage in global toy supply chains.

Top companies operating in the market include:

• Berry Global

• Graphic Packaging International

• Smurfit Kappa

• DS Smith

• Amcor

Other notable companies include Nine Dragons Paper, Greatview Packaging, Toppan, Rengo Co. Ltd., ITC Packaging, Mondi Group, and WestRock.

Outlook: Future of the Licensed Character Packaging for Toddler Toys Market

The future of the licensed character packaging market will be shaped by the continued expansion of character-driven product portfolios and the increasing strategic role of packaging in retail merchandising and regulatory compliance. As brands scale licensed toy programs globally, packaging suppliers that can deliver standardized, repeatable packaging systems will play a central role in supporting rapid SKU expansion and omnichannel distribution models.

Future growth drivers include:

• Technology advancement in print and packaging engineering

• Sustainability initiatives and recyclable packaging materials

• Manufacturing expansion across emerging economies

• Supply chain innovation supporting omnichannel retail

For an in-depth analysis of evolving industry trends and to access the complete strategic outlook for the market through 2036, visit the official report page at: https://www.futuremarketinsights.com/reports/licensed-character-packaging-for-toddler-toys-market