The Pharmaceutical Glass Packaging Market is projected to grow steadily as global pharmaceutical manufacturing expands and regulatory requirements for drug safety become increasingly stringent. The market is valued at USD 8.7 billion in 2026 and is forecast to reach USD 14.2 billion by 2036, progressing at a CAGR of 5.1% during the forecast period. Rising production of injectable drugs, vaccines, and specialty pharmaceuticals is reinforcing the demand for high-quality glass packaging solutions that ensure chemical stability and sterility.

Quick Stats: Pharmaceutical Glass Packaging Market (2026–2036)

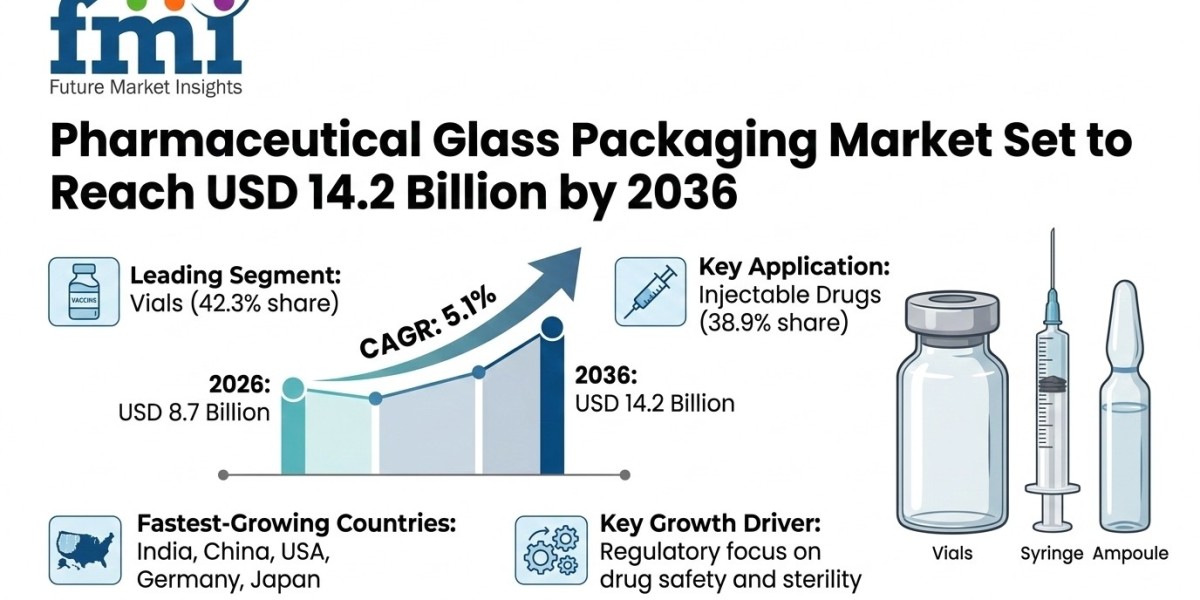

• Market Value (2026): USD 8.7 Billion

• Forecast Value (2036): USD 14.2 Billion

• CAGR: 5.1%

• Leading Segment: Vials (42.3% share)

• Key Product Segment: Injectable Drug Packaging (38.9% share)

• Fastest-Growing Countries: India, China, United States, Germany, Japan

• Key Growth Driver: Increasing regulatory focus on drug stability, sterility, and chemical compatibility

Structural Growth Driver: Pharmaceutical Safety and Regulatory Compliance

Government regulations surrounding pharmaceutical packaging are a major structural driver of the pharmaceutical glass packaging market. Regulatory authorities across global pharmaceutical markets mandate strict testing, certification, and compliance processes for glass containers used in drug storage and delivery. These frameworks ensure that packaging materials do not chemically interact with drug formulations or compromise pharmaceutical stability.

Key regulatory frameworks and industry standards include:

• Pharmacopeial standards for chemical resistance and hydrolytic stability

• Certification requirements for pharmaceutical packaging materials

• Extractables and leachables compliance guidelines

• Sterilization compatibility and thermal shock resistance standards

• Pharmaceutical manufacturing quality systems and GMP compliance

From Compliance to Industry Transformation

Pharmaceutical packaging manufacturers are evolving beyond basic compliance toward integrated quality management systems that support global drug production. Companies are investing in advanced glass manufacturing technologies, precision forming techniques, and quality assurance processes to deliver packaging materials that meet evolving pharmaceutical industry standards.

Companies across the industry are prioritizing:

• Sustainability performance in glass manufacturing

• Cost efficiency in high-volume pharmaceutical packaging production

• Recyclability and circular material utilization

• Compatibility with automated pharmaceutical filling systems

• Reliable sterilization and contamination prevention capabilities

Technology Transformation: Advanced Pharmaceutical Glass Engineering

Technological advancements in glass engineering and pharmaceutical manufacturing processes are improving the performance of pharmaceutical glass packaging. Modern container designs focus on enhanced chemical durability, improved thermal resistance, and greater mechanical strength to support demanding pharmaceutical applications.

Manufacturers are also integrating automation and precision manufacturing technologies to improve container consistency, reduce defects, and maintain strict dimensional tolerances required for pharmaceutical filling lines. These innovations support large-scale drug production while ensuring packaging reliability across diverse pharmaceutical formulations.

Key innovation areas include:

• Advanced pharmaceutical-grade glass material development

• Automation integration in glass forming and inspection

• Lightweight container design for improved logistics efficiency

• Sustainable glass manufacturing and energy-efficient production

• Manufacturing precision and defect detection technologies

Segment Highlights

By Product Type

• Vials (42.3% share): Widely used for injectable drug packaging, vaccine storage, and diagnostic sample collection requiring sterility and chemical stability.

• Bottles (28.4% share): Common in oral medication packaging and liquid formulation storage applications.

• Syringes (16.7% share): Increasingly adopted for pre-filled drug delivery systems and vaccination programs.

• Ampoules (8.9% share): Used for single-dose sterile drug packaging and specialized pharmaceutical treatments.

• Other Containers (3.7% share): Includes cartridges and specialized pharmaceutical glass packaging solutions.

By Application

• Injectable Drugs (38.9% share): Dominates due to strict sterility requirements and rapid expansion of vaccine and biologic drug production.

• Oral Medications (31.2% share): Supports packaging of tablets, capsules, and liquid drug formulations.

• Topical Preparations (18.6% share): Used for creams, ointments, and dermatological pharmaceutical products.

• Diagnostics (7.8% share): Glass containers support reagent storage and medical testing sample collection.

• Other Applications (3.5% share): Includes specialty pharmaceutical packaging and research laboratory use.

Regional Outlook: Emerging Economies Drive Adoption

Global demand for pharmaceutical glass packaging is increasing across both developed and emerging pharmaceutical manufacturing markets. Expanding drug production capacity, biopharmaceutical innovation, and regulatory compliance requirements are accelerating adoption of high-performance glass packaging solutions worldwide.

• India (6.8% CAGR): Growth driven by expanding pharmaceutical manufacturing capacity and rising export-oriented drug production.

• China (6.2% CAGR): Strong demand from biopharmaceutical production and healthcare infrastructure expansion.

• United States (5.4% CAGR): Increasing adoption in specialty drug manufacturing and biologic packaging applications.

• Germany (4.9% CAGR): Growth supported by advanced pharmaceutical production facilities and strong regulatory compliance standards.

• Japan (4.6% CAGR): Demand driven by high-quality pharmaceutical manufacturing and precision packaging requirements.

Risk Landscape: Market Constraints and Challenges

Despite steady growth prospects, the pharmaceutical glass packaging market faces several operational and economic challenges that can influence long-term expansion.

Key market risks include:

• Raw material price volatility in specialty glass production

• Supply chain disruptions affecting pharmaceutical packaging materials

• Infrastructure gaps in emerging pharmaceutical manufacturing markets

• Regulatory complexity across international pharmaceutical markets

• High manufacturing costs associated with pharmaceutical-grade glass production

Competitive Landscape: Key Market Players

Competition in the pharmaceutical glass packaging market is shaped by technological capability, regulatory compliance expertise, and long-term supply partnerships with pharmaceutical manufacturers. Leading companies focus on precision glass manufacturing, advanced container engineering, and integrated packaging solutions designed to meet strict pharmaceutical industry requirements.

Top companies operating in the market include:

• Schott AG

• Gerresheimer AG

• West Pharmaceutical Services

• Bormioli Pharma

• SGD Pharma

Other notable companies include Corning Incorporated, Ardagh Group, Stevanato Group, Nipro Corporation, Piramal Glass, and O-I Glass.

Outlook: Future of the Pharmaceutical Glass Packaging Market

The pharmaceutical glass packaging market is expected to continue expanding as global pharmaceutical production scales and regulatory oversight of drug packaging intensifies. Growing adoption of biologics, injectable drugs, and specialty pharmaceuticals will further strengthen demand for high-quality pharmaceutical-grade glass containers.

Future growth drivers include:

• Technology advancement in pharmaceutical glass manufacturing

• Sustainability initiatives in glass production

• Expansion of pharmaceutical manufacturing facilities

• Supply chain innovation in global drug distribution networks

For an in-depth analysis of evolving industry trends and to access the complete strategic outlook for the market through 2036, visit the official report page at: https://www.futuremarketinsights.com/reports/pharmaceutical-glass-packaging-market