The global alternative hydrocolloids market is projected to grow from USD 2,380.0 million in 2026 to USD 4,467.6 million by 2036, registering a CAGR of 6.5% during the forecast period. Growth is being driven by increasing substitution of conventional hydrocolloids due to supply volatility, pricing instability, and formulation limitations, alongside rising demand for clean-label and plant-based ingredients.

Alternative hydrocolloids such as tara gum, konjac glucomannan, cellulose-based systems, and seaweed-derived variants are gaining traction across dairy alternatives, ready meals, bakery, and beverage applications. Their ability to deliver viscosity, gelling, and water-binding functionality while aligning with consumer-friendly labeling is accelerating adoption globally.

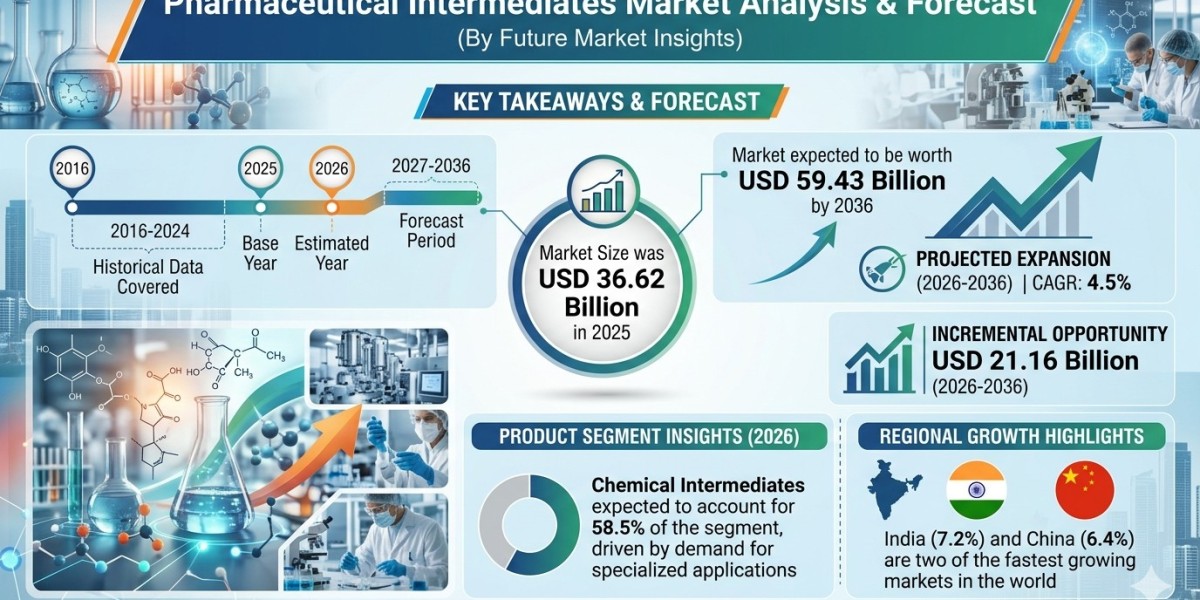

Request Sample Report: https://www.futuremarketinsights.com/reports/sample/rep-gb-31456

Rising Demand for Clean-Label and Functional Ingredients

• Clean-label reformulation: Increasing preference for natural, transparent ingredient sourcing

• Plant-based growth: High demand in dairy alternatives and plant-based food formulations

• Texture optimization: Enhanced viscosity, stability, and mouthfeel across applications

Hydrocolloid Categories and Functional Roles Shape Demand

Key segments are influencing market expansion patterns.

• Tara gum dominance: Leads with strong functional similarity and versatility

• Functional roles: Thickening and viscosity control account for major demand share

• Application diversity: Dairy alternatives, ready meals, and bakery drive utilization

Supply Volatility and Functional Constraints Influence Market Dynamics

• Raw material instability: Fluctuating supply of conventional gums accelerates substitution

• Functional limitations: Hydration behavior and protein interaction impact formulation choices

• Regulatory considerations: Labeling standards and ingredient classification affect scalability

Regional Highlights

• India (7.6% CAGR): Growth driven by local sourcing and thermal stability needs

• China (7.3% CAGR): Rising adoption in high-volume industrial food processing

• Brazil (6.9% CAGR): Demand supported by climate-driven texture stability requirements

• USA (5.8% CAGR): Expansion driven by clean-label reformulation and supply chain diversification

• UK (5.6% CAGR): Growth influenced by regulatory compliance and ingredient transparency

Competitive Landscape

The market is characterized by global ingredient suppliers focusing on innovation, supply reliability, and application-specific solutions.

• Cargill & Ingredion: Broad portfolios with integrated hydrocolloid systems

• ADM & Tate & Lyle: Focus on scalable, process-tolerant ingredient solutions

• CP Kelco: Specialization in high-performance hydrocolloids for complex formulations

Recent Developments

• Increased investment in fermentation-derived and plant-based hydrocolloids

• Advancements in extraction and purification technologies for tailored functionality

• Expansion of application-specific solutions for high-protein and plant-based foods

Analyst Outlook

The alternative hydrocolloids market is expected to witness sustained growth as food manufacturers increasingly prioritize formulation flexibility, clean-label positioning, and supply chain resilience. Adoption will remain application-specific, with innovation focused on improving texture stability and processing performance.

Future Opportunities

• Expansion in plant-based and dairy alternative formulations

• Growth in high-protein and fortified food applications

• Development of multifunctional hydrocolloid systems

• Advancements in sustainable sourcing and fermentation technologies