Market Overview:

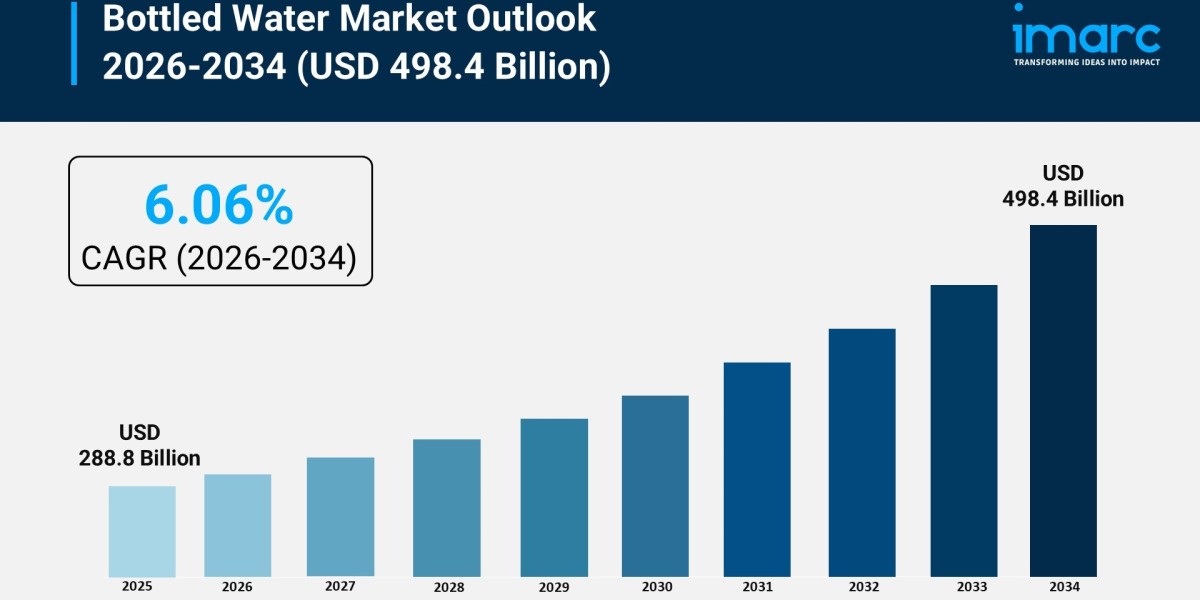

The bottled water market is experiencing rapid growth, driven by increased health and wellness consciousness, lack of reliable public water infrastructure, and on-the-go convenience and lifestyle integration. According to IMARC Group’s latest research publication, “Bottled Water Market Size, Share, Trends and Forecast by Product Type, Distribution Channel, Packaging Type, and Region, 2026-2034”, the global bottled water market size was valued at USD 288.8 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 498.4 Billion by 2034, exhibiting a CAGR of 6.06% during 2026-2034.

This detailed analysis primarily encompasses industry size, business trends, market share, key growth factors, and regional forecasts. The report offers a comprehensive overview and integrates research findings, market assessments, and data from different sources. It also includes pivotal market dynamics like drivers and challenges, while also highlighting growth opportunities, financial insights, technological improvements, emerging trends, and innovations. Besides this, the report provides regional market evaluation, along with a competitive landscape analysis.

Download a sample PDF of this report: https://www.imarcgroup.com/bottled-water-market/requestsample

Our report includes:

- Market Dynamics

- Market Trends and Market Outlook

- Competitive Analysis

- Industry Segmentation

- Strategic Recommendations

Growth Factors in the Bottled Water Market

- Inadequate Public Water Infrastructure and Urbanization

The rapid pace of global urbanization has significantly outstripped the capacity of municipal water systems, particularly in emerging economies where centralized infrastructure remains inconsistent. As highlighted in recent bottled water market research, in many urban centers across Asia and Africa, the perceived or actual contamination of tap water makes bottled alternatives a biological necessity rather than a luxury. For instance, in 2026, the global bottled water market is valued at approximately USD 385 billion, with a substantial portion of this demand stemming from regions like India and China where urban populations frequently encounter service unreliability and groundwater depletion. To bridge this gap, private enterprises have scaled operations to ensure accessibility. A notable example is the widespread adoption of 20-liter bulk jars for home consumption, which provide a reliable primary water source for households in areas where government-supplied piped water is either non-existent or fails to meet safety standards.

- Heightened Health Awareness and Sugar Reduction

A fundamental shift in consumer behavior toward health and wellness is a primary catalyst for industry expansion. Modern consumers are increasingly replacing calorie-dense carbonated soft drinks with bottled water to mitigate lifestyle-related health issues such as obesity and diabetes. Public health reports from organizations like the World Health Organization highlight a global rise in obesity, which has inadvertently bolstered the "better-for-you" beverage segment. In 2026, still bottled water maintains its dominance, accounting for roughly 58% of the total market share, as it is viewed as the ultimate clean-label product. Major beverage corporations have responded by pivoting their portfolios; for example, companies are aggressively marketing mineral-rich and pH-balanced variants to satisfy the demands of health-conscious demographics who prioritize purity and functional hydration over traditional refreshments.

- Strategic Corporate Expansion and Distribution Innovations

The aggressive expansion of retail and e-commerce distribution channels has made bottled water more accessible than ever before. Leading industry players are utilizing direct-to-consumer (DTC) models and subscription-based delivery services to capture at-home consumption trends. In 2026, offline channels—including supermarkets and convenience stores—remain powerful, holding a 69% share of distribution, but the integration of digital procurement is streamlining the supply chain. Companies like Bisleri and Coca-Cola have implemented real-time analytics and blockchain-based traceability to enhance inventory management and transparency. Furthermore, strategic acquisitions, such as Clear Premium Water’s purchase of Kelzai Volcanic Water, demonstrate how firms are diversifying their offerings to include high-margin, niche products like volcanic spring water, thereby capturing both mass-market and premium consumer segments globally.

Key Trends in the Bottled Water Market

- The Rise of Functional and Electrolyte-Enhanced Water

Basic hydration is no longer the sole requirement for a growing segment of the market; instead, consumers are seeking "performance water" tailored to specific wellness goals. This trend is characterized by the infusion of vitamins, minerals, and adaptogens into standard bottled offerings. In 2026, the functional and flavored water sub-segment is seeing significant traction, particularly among fitness enthusiasts and the aging population. Products now feature specialized additives like magnesium for stress relief or caffeine-free botanical extracts for mental clarity. Real-world applications include the launch of alkaline and electrolyte-infused variants designed to assist with post-exercise recovery. Brands are increasingly positioning these as essential lifestyle tools rather than just beverages, allowing them to command higher price points in both developed and emerging markets.

- Sustainability and Circular Packaging Models

Environmental consciousness is fundamentally reshaping packaging strategies as brands move away from traditional single-use plastics. The industry is witnessing a massive transition toward 100% recycled PET (rPET), aluminum cans, and biodegradable materials to align with stringent government regulations on plastic waste. For example, major players have introduced fully recyclable paper-based cartons and lightweight bottles that utilize plant-based polymers to reduce carbon footprints. In 2026, PET bottles still lead with a 64% share of the packaging format, but there is a distinct surge in "circular economy" initiatives. Companies are now implementing closed-loop recycling programs where they collect used bottles to manufacture new ones, responding directly to the demands of Gen Z and millennial consumers who prioritize brands with verifiable eco-friendly credentials.

- Premiumization and Source Transparency

Consumers are increasingly willing to pay a premium for water with a "story," leading to a trend of highlighting unique geographical origins and mineral profiles. Whether it is glacier-sourced water from the Alps or volcanic water from the Himalayas, the source has become a key differentiator. This trend is supported by the growth of the premium segment, which is projected to reach USD 39 billion in 2026. High-end hotels and fine-dining establishments are fueling this demand by offering "water menus" that feature artisanal brands with specific pH levels and TDS (Total Dissolved Solids) counts. Brands are using QR codes on labels to provide consumers with instant access to lab reports and digital tours of the water source, catering to a sophisticated demographic that values transparency and the perceived health benefits of naturally filtered water.

Leading Companies Operating in the Global Bottled Water Industry:

- Bisleri International Pvt. Ltd.

- Danone S.A.

- Gerolsteiner Brunnen GmbH & Co. KG

- Nestle S.A.

- Nongfu Spring (Yangshengtang Co. Ltd.)

- Otsuka Pharmaceutical Co. Ltd.

- PepsiCo Inc.

- Primo Water Corporation

- Tata Consumer Products Limited

- The Coca-Cola Company

Bottled Water Market Report Segmentation:

By Product Type:

- Still

- Carbonated

- Flavored

- Mineral

Still bottled water dominates the market in 2024 with a 55.8% share, driven by health awareness and demand for hydration.

By Distribution Channel:

- Supermarkets/Hypermarkets

- Convenience Stores

- Direct Sales

- On-Trade

- Others

Supermarkets and hypermarkets lead distribution with 59.4% market share in 2024, offering extensive variety and convenience for consumers.

Packaging Type:

- PET Bottles

- Metal Cans

- Others

PET bottles hold an 80.0% market share in 2024 due to their recyclability and availability in various sizes, enhancing environmental friendliness.

Regional Insights:

- North America (United States, Canada)

- Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, Others)

- Europe (Germany, France, United Kingdom, Italy, Spain, Russia, Others)

- Latin America (Brazil, Mexico, Others)

- Middle East and Africa

Asia-Pacific leads the bottled water market in 2024 with over 44.5% share, fueled by urbanization, rising incomes, and concerns over water-borne diseases.

Note: If you require specific details, data, or insights that are not currently included in the scope of this report, we are happy to accommodate your request. As part of our customization service, we will gather and provide the additional information you need, tailored to your specific requirements. Please let us know your exact needs, and we will ensure the report is updated accordingly to meet your expectations.

About Us:

IMARC Group is a global management consulting firm that helps the world’s most ambitious changemakers to create a lasting impact. The company provide a comprehensive suite of market entry and expansion services. IMARC offerings include thorough market assessment, feasibility studies, company incorporation assistance, factory setup support, regulatory approvals and licensing navigation, branding, marketing and sales strategies, competitive landscape and benchmarking analyses, pricing and cost research, and procurement research.

Contact Us:

IMARC Group

134 N 4th St. Brooklyn, NY 11249, USA

Email: sales@imarcgroup.com

Tel No:(D) +91 120 433 0800

United States: +1-201971-6302